Market Quick Hits

- Solid July for Markets

- Continued Challenges for Fixed Income

- Economic Growth Beats Expectations

- Market Risks Fading

- Strong Economy Supports Positive Outlook

Solid July for Markets

Equity markets rallied in July, with rising investor confidence helping to support stocks to start the second half of the year. The S&P 500 rose 3.21 percent during the month while the Dow Jones Industrial Average gained 3.44 percent. The Nasdaq Composite led the way with a 4.08 percent gain as technology stocks continued to rally. These positive results helped bring all three indices near their respective all-time highs that were set in late 2021 and early 2022.

While results were encouraging, market fundamentals showed signs of a slowdown in certain sectors. Per Bloomberg Intelligence, as of July 31, 2023, with 53 percent of companies having reported actual earnings, the blended earnings decline for the S&P 500 was 9.1 percent—slightly worse than the 9.0 percent drop expected at the start of earnings season. The weakness was largely concentrated in the energy and materials sectors, but a larger-than-expected decline in health care earnings also contributed to the overall drop in quarterly earnings. Fundamentals drive long-term performance, so this will be an important area to monitor.

Unlike fundamental factors, technical factors were supportive. All three major U.S. indices finished the month well above their respective 200-day moving averages for the seventh consecutive month. The 200-day moving average is a widely followed technical signal, as prolonged breaks above or below this level can signal shifting investor sentiment for an index.

International markets were a similar story in July. The MSCI EAFE Index gained 3.24 percent while the MSCI Emerging Markets Index surged 6.29 percent. These positive results ensured that technical factors remained supportive, with both indices finishing above their respective 200-day moving averages in July.

Ongoing Challenges for Fixed Income

While stocks continued to rally to start the second half of the year, the same can’t be said for bonds. Rising rates weighed on bond prices, with the 10-year U.S. Treasury yield rising from 3.81 percent at the end of June to 3.97 percent at the end of July. The Bloomberg Aggregate Bond Index lost 0.07 percent.

The Federal Reserve (Fed) hiked the federal funds rate 25 basis points (bps) at its July meeting, which was widely anticipated by investors and economists. While the hike was expected due to the Fed’s fight against inflation, the major takeaway from the meeting was that the Fed no longer expects to see the economy enter into a recession in the near future. This positive revision to the Fed’s outlook suggests the central bank is unlikely to hike rates again at its September meeting and could even signal an end to the Fed’s current rate hiking cycle.

High-yield fixed income, which typically performs well when equity markets rally, saw gains in July. The Bloomberg U.S. Corporate High Yield Index gained 1.38 percent. High-yield bond returns were supported by falling credit spreads. Spreads dropped from 4.14 percent at the end of June to 3.82 percent at the end of July. Falling spreads signal growing investor appetite for investing in higher-yield securities and help support prices for existing bonds.

Economic Growth Beats Expectations

Economic updates released in July showed signs of better-than-expected growth across the economy. The first look at second-quarter GDP growth showed that the economy grew at an annualized rate of 2.4 percent during the quarter, well above the 1.8 percent that was expected. This growth was supported by improved consumer confidence and spending.

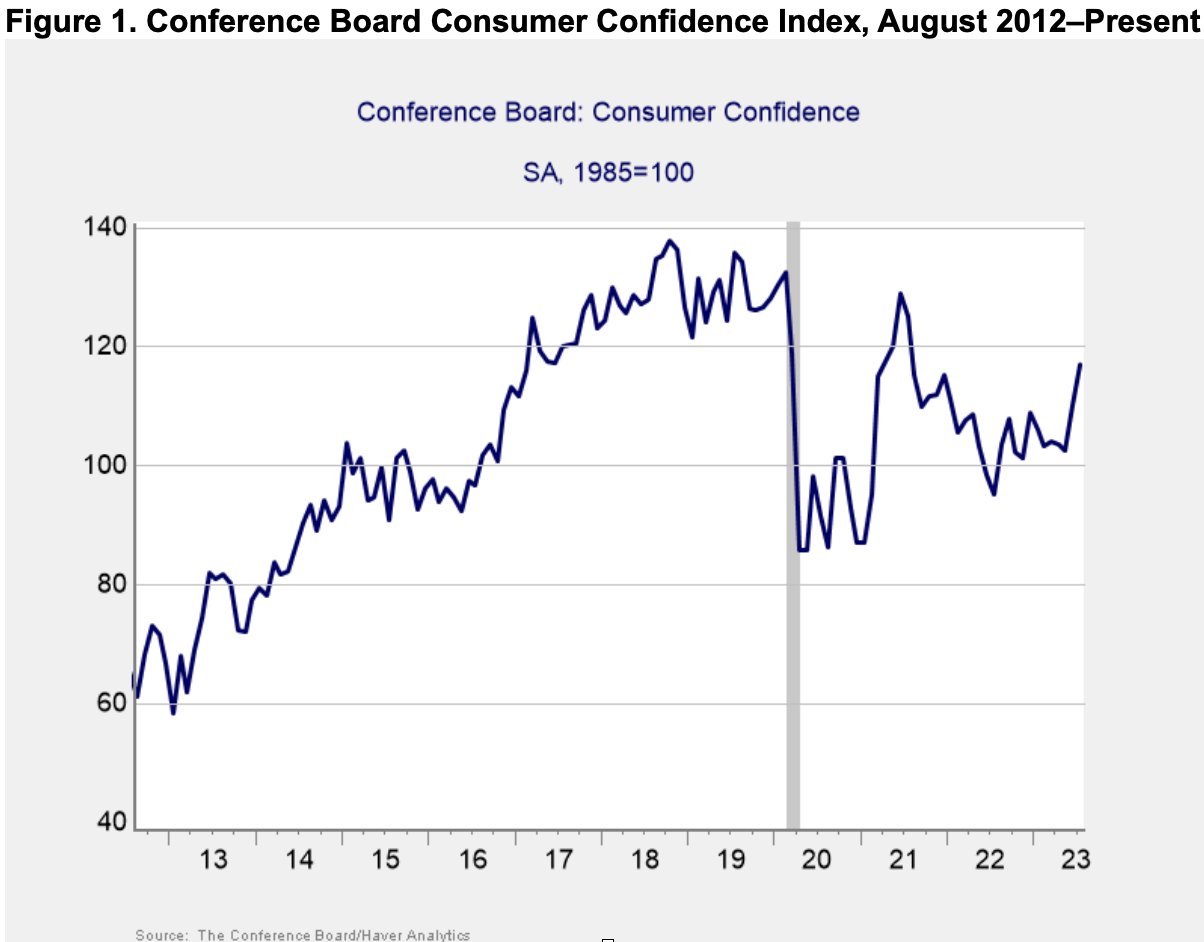

Consumer sentiment improved notably in July, with both major measures of consumer confidence coming in better than expected during the month. As you can see in Figure 1, the Conference Board Consumer Confidence Index now sits at its highest level in two years.

The increasing confidence was supported by rising optimism on current economic conditions, with the present subindex hitting its highest level since the start of the Covid-19 pandemic during the month. While there is still work to be done to get headline confidence back to pre-pandemic levels, the improvements in July suggest that we’re on the right track.

Strong job creation in the first half of the year supported the rise in confidence that we’ve seen in 2023 so far. June’s employment report showed that 209,000 jobs were added during the month, which drew unemployment down to 3.6 percent and highlighted the strength of the labor market.

Perhaps the most impressive feature of the current economic expansion is the fact that we continue to see signs of solid growth combined with declining inflation. Annual consumer inflation fell to 3 percent in June 2023 after peaking at 9.1 percent in June 2022, highlighting notable progress in combating inflationary pressure over the past year.

Although the Fed did still announce a 25 bps hike at its July meeting, markets do not expect any further rate hikes for the rest of the year. While this outlook could certainly change if we see an uptick in inflation or notable weakness from the job market, in general, the Fed’s impact on the economy and markets may be set to swing from restrictive to supportive in the second half of this year or early 2024. For now, inflation and the Fed will still be closely monitored by investors and economists given the importance of both for markets. But the developments we’ve seen on the inflation front this year are encouraging.

The Takeaway

- July showed continually strong economic growth to start the second half of the year.

- Inflation also showed better-than-expected signs of improvement during the month.

Market Risks Fading

The first half of the year saw a number of risks negatively impact markets; however, most of the initial impact has since faded. The debt ceiling standoff at the end of May and start of June is a good example, as we’ve seen markets rally notably since the successful resolution of the standoff. Additionally, concerns around the banking sector have cooled notably since March, and markets have largely shrugged off the initial volatility associated with both risk factors.

Looking forward, there are still very real risks that should be monitored. Domestically, the primary risk is that inflation could spike again if growth continues to come in above expectations, which could lead to further unexpected rate hikes. While this does not appear to be an immediate concern given the recent progress we’ve seen in lowering inflationary pressure, it’s certainly possible and should be monitored as unexpected hikes could negatively impact both stock and bond valuations.

International risks remain, as evidenced by the ongoing war between Russia and Ukraine as well as concerns surrounding a slowdown in China. While the immediate market impact from these risk factors is limited, these are areas of potential concern that could lead to further uncertainty for investors.

Finally, there are also the unknown risks that we can’t predict at this time, which always have the potential to negatively impact markets.

The Takeaway

- Inflation and the Fed are the primary domestic risks, although signs point toward continued improvements on the inflation front.

- International and unknown risks remain and should be monitored.

Strong Economy Supports Positive Outlook

Despite the real risks that markets face, the strong economy is a tailwind for investors. Better-than-expected economic news to start the second half of the year continued to paint a picture of a healthy economic expansion, which should support stock prices. With many primary risks from earlier in the year receding, the outlook for the rest of the year is positive for both markets and the economy.

Of course, while economic growth and market appreciation are the most likely path forward, there is potential for short-term disruptions. A well-diversified portfolio that matches investor timelines and goals remains the best path forward for most. As always, you should reach out to your financial advisor to discuss your current plan if you have concerns.

The Takeaway

- Continued economic growth is expected to help support markets in the months ahead.

- Over the long run, the outlook remains positive, with potential for short-term setbacks.

Disclosures: Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. All indices are unmanaged and are not available for direct investment by the public. Past performance is not indicative of future results. The S&P 500 is based on the average performance of the 500 industrial stocks monitored by Standard & Poor’s. The Nasdaq Composite Index measures the performance of all issues listed in the Nasdaq Stock Market, except for rights, warrants, units, and convertible debentures. The Dow Jones Industrial Average is computed by summing the prices of the stocks of 30 large companies and then dividing that total by an adjusted value, one which has been adjusted over the years to account for the effects of stock splits on the prices of the 30 companies. Dividends are reinvested to reflect the actual performance of the underlying securities. The MSCI EAFE Index is a float-adjusted market capitalization index designed to measure developed market equity performance, excluding the U.S. and Canada. The MSCI Emerging Markets Index is a market capitalization-weighted index composed of companies representative of the market structure of 26 emerging market countries in Europe, Latin America, and the Pacific Basin. The Russell 2000® Index measures the performance of the 2,000 smallest companies in the Russell 3000® Index. The Bloomberg US Aggregate Bond Index is an unmanaged market value-weighted performance benchmark for investment-grade fixed-rate debt issues, including government, corporate, asset-backed, and mortgage-backed securities with maturities of at least one year. The U.S. Treasury Index is based on the auctions of U.S. Treasury bills, or on the U.S. Treasury’s daily yield curve. The Bloomberg US Mortgage Backed Securities (MBS) Index is an unmanaged market value-weighted index of 15- and 30-year fixed-rate securities backed by mortgage pools of the Government National Mortgage Association (GNMA), Federal National Mortgage Association (Fannie Mae), and the Federal Home Loan Mortgage Corporation (FHLMC), and balloon mortgages with fixed-rate coupons. The Bloomberg US Municipal Index includes investment-grade, tax-exempt, and fixed-rate bonds with long-term maturities (greater than 2 years) selected from issues larger than $50 million. One basis point is equal to 1/100th of 1 percent, or 0.01 percent.

Authored by Brad McMillan, CFA®, CAIA, MAI, managing principal, chief investment officer, and Sam Millette, director, fixed income, at Commonwealth Financial Network®.

© 2023 Commonwealth Financial Network